On this episode, I’m joined by a quant trader who works at a high frequency trading firm—though you might be surprised to hear, he started out on the same path that many retail traders do—his name is; Dave Bergstrom.

The thing that makes Dave unique from most traders who’ve been on this podcast previously, is how he uses data-mining techniques to develop trading strategies. Though data-mining, in trading, often has a negative connotation attached to it, Dave believes this stems from bad practices and poor evaluation of methods.

In addition to the above and ways to reduce curve-fitting, we talk about escaping randomness, learning to write code, Dave’s three laws for strategy development, setting expectations and plenty more.

Q+A: Got a question for Dave? Write in the comments area at the bottom of this page.

Topics of discussion:

- Dave explains why he couldn’t “escape randomness” in the beginning, how he landed a position in a HFT firm, and why he became more data-driven as a trader.

- The reasons why Dave learned how to program (in multiple languages) and how it’s comparable to having “superpowers”, plus a few tips for learning the basics.

- Should data-mining be avoided? Dave shares a high-level overview for how he finds an edge by mining data and the measures he takes to reduce curve fitting.

- Dave’s “three trading laws” for strategy development, the benefits of variance testing, and how Monte Carlo analysis can help to set realistic expectations.

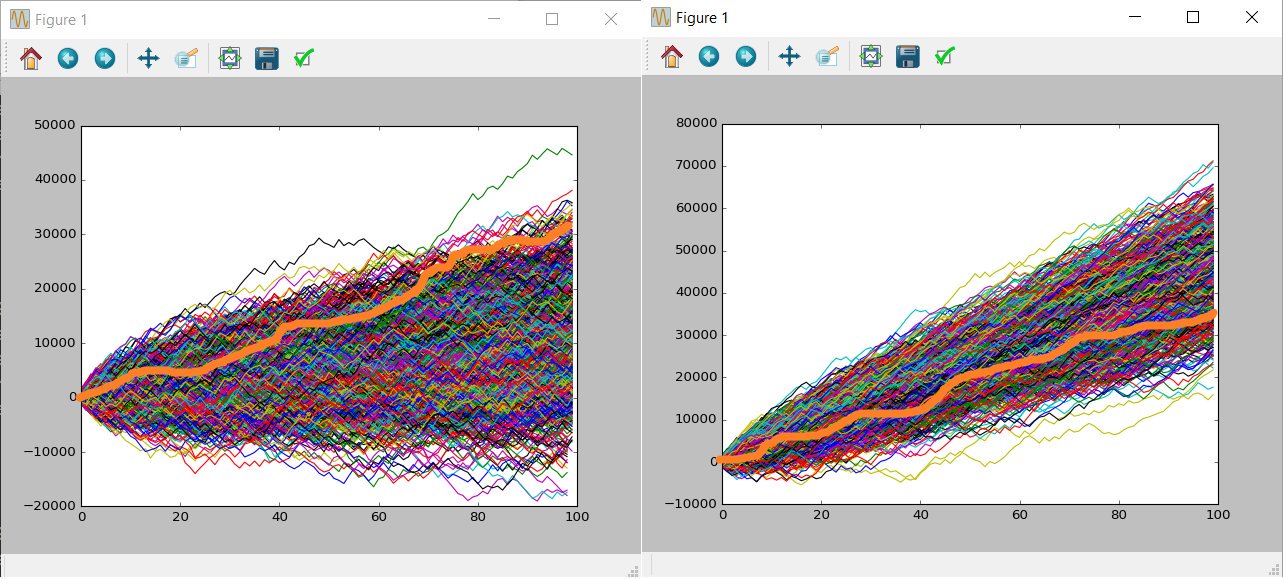

“Assume orange is your backtest (same in both pics) but makes a big difference which distribution it came from.” Tweet by @DBurgh

Links and resources mentioned:

- BuildAlpha.com

- Evidence-Based Technical Analysis, by David Aronson

- StackOverflow.com

- Coursera.com

- @DBurgh

How to support this podcast:

- For a quick and easy way to support this free podcast, please write an honest review in iTunes. It’ll take you two minutes, and it helps massively—thank you.