All episodes of Chat With Traders x Quantopian mini-series are available here.

When one has a price model that they think will work well for forecasting returns, the next step is to actually trade it. This isn’t that simple for a variety of reasons. For one thing, you need to define how much risk you’re okay with taking on in a portfolio, and then try to maximize your returns while staying within those boundaries. This is the foundation of modern portfolio theory—we’ll discuss some real life issues with this.

Sponsored by DataCamp:

- Wanna learn how to code? Then you best visit DataCamp.com. They’ve got a full suite of data science courses that’ll give you the skill-sets necessary of a quant.

Topics of discussion:

- The need to spread capital beyond a single asset and the notion of optimization.

- Optimizing for maximum returns within your portfolio constraints.

- Implicit assumptions that can creep in during portfolio optimization.

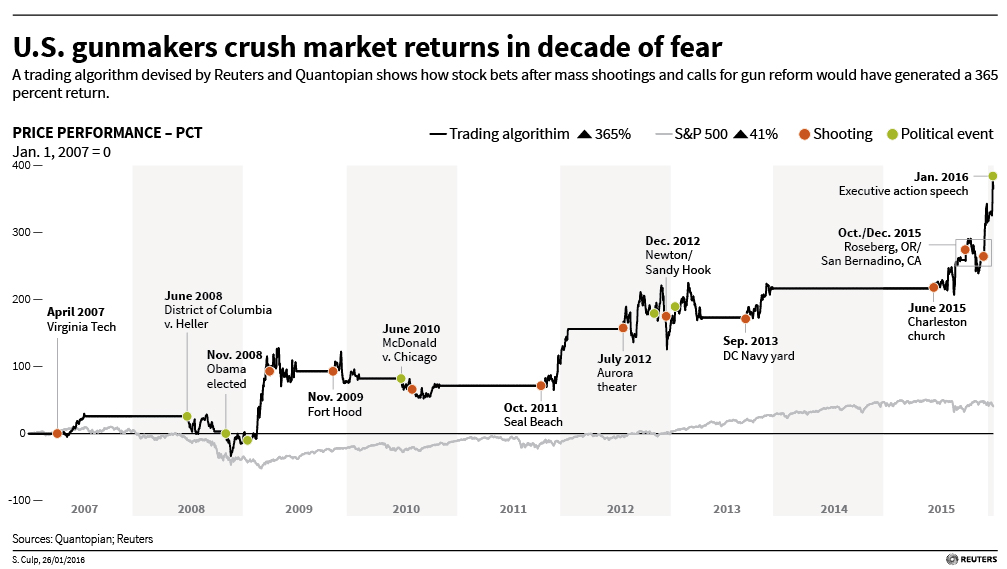

- How an example strategy, trading gun manufacturers, could be optimized.

Click image to view full size.

Links and resources mentioned:

- Intro to Optimization (Wikipedia)

- Optimization API (Quantopian forum)

- Portfolio Optimization (Jupyter notebook)

- Real returns vs normal distributions (Quantopian lecture)

- How mass shootings and politics boost gun shares (Quantopian forum)

- Trading algorithm shows how mass shootings, politics boost gun shares (Reuters)

- @ScottBSanderson (Twitter)

How to support this podcast:

- For a quick and easy way to support this free podcast, please write an honest review in iTunes. It’ll take you two minutes, and it helps massively—thank you.